Its hard for active managers to outperform passive. Yet one area provides an opportunity: emerging markets. It turns out a simple trick can help boost performance when compared to standard emerging market benchmarks. The trick is to avoid State Owned Enterprises.

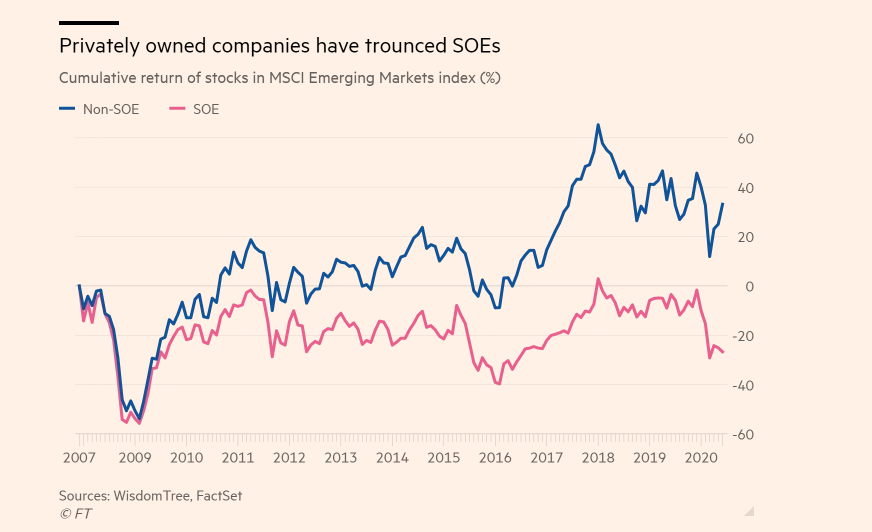

Here is a chart from the FT showing how much better private companies in emerging markets perform.

Several analysts provided background on why SOEs underperform. SOEs are typically run by bureaucrats or politicians, not entrepreneurs. Often they are incentivized to provide jobs, or serve some other social function, rather than earn profits. In some cases SOEs are used as personal piggy banks of corrupt politicians.

According to Emily Leveille, EM equity portfolio manager at Nordea Asset Management:

SOEs tend to underperform over time because management often have a mandate that is not necessarily aligned with maximising returns for minority shareholders. They have state goals,” said Emily Leveille, EM equity portfolio manager at Nordea Asset Management.

According to Kevin Carter, who runs the Emerging Markets Internet and E-commerce Fund (EMQQ) an ETF focused on consumer technology companies in emerging markets:

These are not really companies. They are full of fraud, conflicts of interest and corruption. They don’t really care about growing earnings and maximizing shareholder value, so why would you invest in them?”

Most SOEs are also in industries that aren’t in profitable industries. SOEs typically dominate strategic sectors with low returns on equity. Non-SOEs typically operate in dynamic, high growth industries. According to WisdomTree, approximately 74% of SOEs are in “old economy” industries, such as energy, financial ,materials, real estate and utilities, while the remainder is in new economy industries such as consumer services, consumer discretionary, staples, healthcare, and technology. With non-SOE companies in emerging markets, the percentages are reversed. Most EM strategists don’t expected this to change.

Other analysis argue that more nuance is needed. According to Gordon Yeo, portfolio manager at the Arisaig Asia Consumer Fund, generalizations can be deceptive. Most SOEs perform poorly, but there might be important exceptions that investors could miss if they are overly dogmatic.

ETFs that exclude State Owned Enterprises

There is one broad based Emerging Market ETF that avoids state owned enterprises: the Wisdom Tree Emerging Markets ex State-Owned Enterprises Fund (XSOE). XSOE returned an annualized 13% over the past five years, well above the median EM ETF return. According to Morningstar, this is the third Highest out of 82 EM ETFS.

Additionally, there is one niche ETF that avoids state owned enterprises: The Emerging Markets Internet and E-commerce Fund (EMQQ). After a slow start in 2014, EMQQ raised over $500 million in even as it charged 0.86% (compared to 0.67% for EEM). It successfully told a story emphasizing rising internet penetration in emerging markets, and how existing emerging market indices didn’t provide adequate exposure to major e-commerce firms in emerging markets. EMQQ only includes internet/ecommerce companies with over 50% of revenue coming from emerging or frontier markets, By avoiding SOEs, EMQQ has also delivered superior returns.

There are probably other non SOE niches that would make great additions to the emerging market ETF universe.